Advice firms have been quietly subsidising their investment process for years. The data on managed accounts adoption suggests how much capacity is sitting on the table for firms that restructure it.

Most advice firms have never measured what their investment function costs. Not in hours, not in dollars. Not broken down by the person doing the work. They know the function is there. They know it takes time. They have not counted it.

The State Street and Investment Trends 2026 Managed Accounts Report, surveying 1,086 advisers, gives a partial view from the other side: around 60% of advisers using managed accounts cite time savings, reduced compliance workload, and improved scalability as primary benefits. 59 per cent said the structures had improved business profitability. Among practices with more than five advisers, 73% now use managed accounts. Among sole advisers, the figure is 54%. This gap is consistent with a finding from the Investment Trends 2025 Adviser Business Model Report (released August 2025): the top 20% of practices charge nearly double the ongoing fees of their peers and run leaner cost-to-serve models doing it.

But those figures describe what firms gained after restructuring. They do not describe what firms are currently spending. The conclusion most readers draw from this kind of data is that managed accounts are an efficiency play. That is true, but it is the second-order conclusion. The first-order question is what those efficiencies are replacing. They are replacing a set of investment functions that advice firms have historically absorbed inside the practice without measuring them.

The argument is not that every advice firm should outsource its investment process or move every client into a managed account. Some firms run sophisticated in-house investment functions and have the resourcing to keep doing so. Others have business models where the investment work is the differentiator and outsourcing it would damage the proposition. The argument is that few firms have actually counted the hours, attached a cost to them, and asked whether the current structure is the best use of practice capacity. Until that audit is done, the question of how to structure the investment function is being answered by inertia rather than analysis.

What follows is a way to think about the audit, the categories of work it should cover, and the practical options for restructuring the function once the data is in.

Investment work in a typical advice firm is distributed across three roles. Advisers spend time on portfolio reviews for client meetings, market commentary, model implementation across individual portfolios, and IC explanations. Principals or heads of investment spend time on APL maintenance, manager meetings, IC preparation and minutes, research review, and portfolio construction. Support staff spend time on rebalancing, trade implementation, fee disclosure, performance reporting and corporate actions. None of this is unusual but all of it adds up.

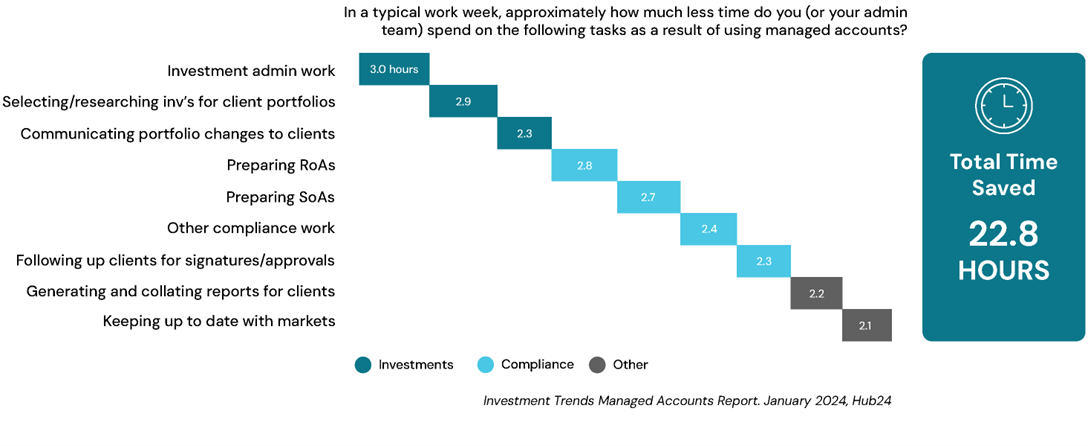

The Investment Trends data on managed account users gives a partial sense of the scale. Among advisers using managed accounts, 25% reported reclaiming more than seven hours a week on portfolio management activities, with a further 28% saving four to six hours, according to separate Praemium research. The earlier SPDR/Investment Trends 2025 Managed Accounts Report put the average at approximately 23 hours saved per week per practice including support staff time. These figures come from vendor-adjacent surveys and should be read as the upper end of the range. The directional finding holds: advisers who restructure their investment implementation reclaim measurable, weekly hours.

Separate research from Elixir Consulting and Lonsec, surveying 171 advisory firms including 561 financial advisers, found that practices with managed accounts across more than 70% of their client base reported the highest efficiency gains, with 63% clawing back up to 10 hours each week.

What the surveys do not capture as cleanly is the time spent on functions that are harder to vacate even when managed accounts are in place: APL governance, manager research, IC documentation, response to regulatory changes like REP 820. These are the functions where the time cost has been growing fastest and where the typical firm has the least dedicated resources.

The audit does not need to be elaborate. Over a representative four-to-six-week period, advisers, the principal, and key support staff log time spent on investment-related work in five categories:

The categories are coarse by design; a defensible total matters more than precision.

Firms typically find a distribution that surprises them. Implementation and reporting often consume more hours than the principal had estimated. Governance often consumes fewer, which is the more concerning finding given the regulatory direction described in REP 820. Client-facing investment work scales with client numbers in non-managed structures, and that scaling cost is one of the most important findings of the audit. If the firm is adding clients faster than it can absorb the implementation load, the structure is failing on capacity grounds before any consideration of governance quality.

The output is a simple table: hours per week by category, multiplied by the loaded cost of the people involved, gives an annualised cost for each function. That figure becomes the benchmark for any restructuring decision.

Once the audit is done, the firm has three categories of options. Each has a different cost profile and a different effect on the function being restructured.

The first is internal restructuring. Reallocate work across existing roles, formalise IC and APL processes to reduce ad-hoc time, build templates and checklists for the recurring tasks, and document the investment process so newer staff can pick it up faster. This is the lowest-cost option and the one that most firms underestimate. A poorly documented investment process is expensive every time someone joins or leaves.

The second is implementation outsourcing. Move client portfolios into a managed account structure (SMA, MDA, or platform-based model portfolio) so that rebalancing, trade implementation, corporate actions and reporting are handled at scale. The State Street/Investment Trends 2026 figures give the order of magnitude: among advisers using managed accounts, 70% cite simplified portfolio management and rebalancing as a key advantage; around 60% cite time savings, reduced compliance workload and improved scalability. This is where most of the visible time savings sit. It is also where the advice firm overlap with super fund-style operating models is most direct.

The third is investment governance outsourcing. Retain external support for the work that managed account implementation does not address: APL construction, manager research, IC support, and the broader governance overlay that the regulatory environment increasingly expects. This is the function asset consultants have provided to institutional investors for several decades and that has, until recently, not been priced or packaged for advice firms of medium size. It is also the function that, for most firms, internal restructuring cannot fully solve, because it requires expertise that does not scale on the size of an advice business.

These options are not mutually exclusive. The most common answer for a 5 to 50 adviser firm is a combination: tighter internal processes, managed account implementation for the majority of client portfolios, and external support on the governance and research functions. The right mix depends on what the audit shows, on the firm’s investment philosophy, and on how the principal wants to use the capacity that the restructuring releases.

Capacity released through investment function restructuring has three plausible uses: redirected to advice and client relationships, redirected to growth, or left in the practice as margin. The Investment Trends 2025 Adviser Business Model Report found that 52% of advisers reported a rise in practice earnings in 2025, with 11% reporting a decline (the lowest level in a decade). The most profitable practices, the report noted, are characterised by higher ongoing fees, leaner cost-to-serve, and greater use of managed accounts to deliver scale. The capacity created by restructuring is not theoretical. It is showing up in the practices that have already done the work.

The decision facing most advice firms over the next year is not whether to make changes to the investment function. The regulatory and competitive pressure described in this article and in our other pieces on REP 820 and the institutional playbook makes that decision largely settled. The decision is whether the changes will be made in response to data the firm has gathered itself, or in response to a regulator, a client complaint, or a competitor whose lower cost-to-serve has eroded the firm’s ability to compete on price.

The firms that will look strongest on the other side of this period are the ones that ran the audit, made the structural calls based on the data, and used the capacity they released to do more of what their advisers are actually paid to do. The investment function is not the work that builds an advice firm’s franchise. It is the work that has historically consumed the time of the people who do.

Sources: